By 2026, Open Banking initiatives in the US are poised to profoundly reshape credit decisions, leveraging secure data sharing to create more accurate and inclusive financial assessments.

Por: Maria Eduarda em 11 de junho de 2026

Última atualização em: 26 de junho de 2026

Advertisements

By 2026, Open Banking initiatives in the US are poised to profoundly reshape credit decisions, leveraging secure data sharing to create more accurate and inclusive financial assessments.

The financial landscape in the United States is on the cusp of a profound transformation, with Open Banking initiatives in the US for 2026: How data sharing will reshape credit decisions in 12 months emerging as a pivotal force. This shift promises to fundamentally alter how individuals and businesses access credit, moving away from traditional, often restrictive models. The integration of secure data sharing protocols is set to unlock unprecedented opportunities for more accurate, personalized, and inclusive credit assessments, benefiting millions of Americans who may currently be underserved by the existing financial system.

Advertisements

The Dawn of Open Banking in the US: A Paradigm Shift

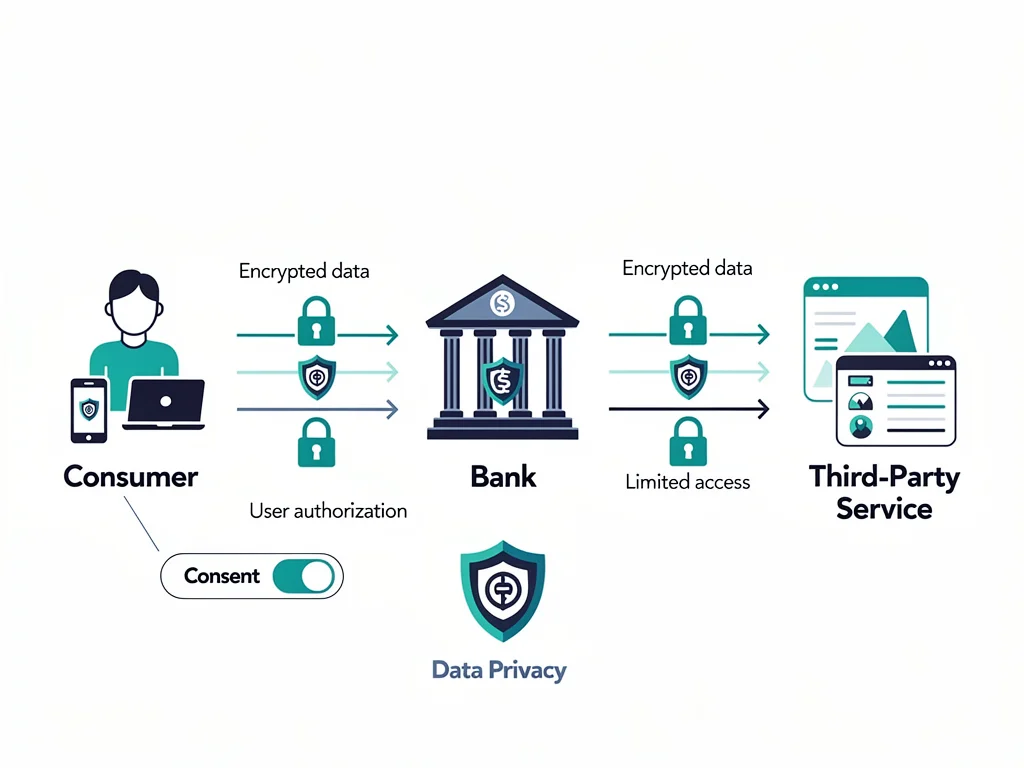

Open Banking, a concept that has already gained significant traction in other global markets, is finally taking root in the United States. This paradigm shift is not merely a technological upgrade; it represents a fundamental rethinking of how financial data is owned, accessed, and utilized. By enabling consumers to securely share their financial data with third-party providers, Open Banking fosters a more competitive and innovative financial ecosystem.

Historically, financial data has been siloed within individual institutions, making it challenging for consumers to leverage their complete financial picture when seeking services like credit. Open Banking breaks down these barriers, empowering individuals with greater control over their financial information. This increased transparency and accessibility are expected to drive a wave of innovation, leading to better products and services tailored to individual needs.

Understanding the Core Principles

At its heart, Open Banking operates on a few core principles. These principles are designed to ensure security, consumer control, and a level playing field for all participants in the financial sector. Adherence to these principles is crucial for the successful implementation and adoption of these new frameworks.

Consumer Consent: Individuals must explicitly grant permission for their data to be shared, retaining the right to revoke access at any time.

Secure APIs: Standardized Application Programming Interfaces (APIs) ensure the secure and efficient transfer of data between authorized parties.

Third-Party Access: Regulated third-party providers can access consumer data, with consent, to offer innovative financial products and services.

Data Portability: Consumers gain the ability to move their financial data seamlessly between different institutions and providers.

In conclusion, the arrival of Open Banking in the US marks a significant turning point. It promises to democratize financial data, placing consumers in the driver’s seat and paving the way for a more dynamic, competitive, and ultimately, more beneficial financial future for everyone. The implications for credit decisions are particularly profound, as lenders will gain access to a richer, more holistic view of an applicant’s financial health.

Regulatory Landscape and Key Drivers for 2026

The advancement of Open Banking in the US is intricately linked to its evolving regulatory landscape. Unlike the UK or Europe, where government mandates have largely driven adoption, the US approach has been more nuanced, characterized by a blend of regulatory encouragement and market-led innovation. However, 2026 is poised to be a critical year, with several key drivers accelerating the pace of change.

The Consumer Financial Protection Bureau (CFPB) has been a significant proponent of data portability, issuing guidance and exploring rules that would formalize consumer data rights. This regulatory push, while not a direct mandate for Open Banking, creates a fertile ground for its development by emphasizing consumer control and access to their own financial information. Financial institutions are increasingly recognizing the strategic advantages of participating in this evolving ecosystem.

CFPB’s Role in Data Portability

The CFPB’s efforts are central to establishing a clear framework for data sharing. Their focus on Section 1033 of the Dodd-Frank Act, which grants consumers the right to access their financial data, is a powerful catalyst. This regulatory interpretation is pushing financial institutions to adopt more standardized and secure methods for data exchange, moving away from less secure practices like screen scraping.

Enhanced Consumer Control: Empowering individuals to manage and direct their financial data.

Standardized Access: Promoting common technical standards for data sharing to ensure interoperability.

Reduced Friction: Streamlining the process for consumers to switch providers or access new services.

Beyond regulation, market forces are also playing a crucial role. Fintech companies, with their agile development and customer-centric approaches, are continuously pushing the boundaries of what’s possible with financial data. Traditional banks, recognizing the competitive threat and the potential for new revenue streams, are also investing heavily in Open Banking capabilities. This dual pressure from regulators and the market is creating a powerful impetus for widespread adoption by 2026.

How Data Sharing Will Reshape Credit Decisions

The most significant impact of Open Banking in the US will undoubtedly be on credit decisions. Traditional credit scoring models, while effective to a degree, often rely on a limited set of historical data points, primarily focusing on past repayment behavior and debt levels. This narrow view can exclude millions of creditworthy individuals who have non-traditional financial profiles or limited credit histories.

Open Banking changes this by providing lenders with a much richer and more granular view of an applicant’s financial health. With consent, lenders can access real-time transaction data, savings patterns, income stability (beyond just reported salary), and even behavioral insights that were previously unavailable. This expanded data set allows for more accurate risk assessments and a more holistic understanding of an individual’s capacity and willingness to repay.

Beyond Traditional Credit Scores

Imagine a scenario where a young professional, new to the country, has no established credit history but demonstrates consistent income, responsible spending habits, and robust savings through their bank accounts. Under traditional models, they might be denied credit or offered unfavorable terms. With Open Banking, a lender could access this data, painting a much clearer picture of their financial responsibility.

Real-time Income Verification: Instant and accurate confirmation of an applicant’s current income streams.

Spending Behavior Analysis: Insights into discretionary spending, bill payment patterns, and financial discipline.

Savings Habits: Evidence of financial prudence and ability to absorb unforeseen expenses.

Debt-to-Income Ratio Refinement: A more precise calculation based on comprehensive data.

Furthermore, Open Banking can help identify predatory lending practices by providing transparency into a consumer’s financial vulnerabilities. The ability to analyze a broader spectrum of financial data will lead to more intelligent lending, benefiting both consumers through fairer access to credit and lenders through reduced risk and more robust portfolios. This shift is not just about technology; it’s about fundamentally improving the fairness and efficiency of the credit market.

Enhanced Financial Inclusion and Accessibility

One of the most compelling aspects of Open Banking’s impact on credit decisions is its potential to significantly enhance financial inclusion. Millions of Americans are considered ‘credit invisible’ or ‘thin-file,’ meaning they have little to no credit history to enable traditional lenders to assess their creditworthiness. This often includes young adults, immigrants, and individuals who primarily use cash or debit cards.

Open Banking provides a pathway for these underserved populations to access credit by allowing alternative data sources to be considered. Instead of solely relying on credit bureau reports, lenders can now, with consent, analyze utility payment history, rental payments, subscription services, and even regular savings contributions. This broader data set can reveal a consistent pattern of responsible financial behavior that traditional models overlook.

Bridging the Credit Gap

The current system often perpetuates a cycle where individuals without credit history struggle to obtain credit, thus preventing them from building a history. Open Banking offers a powerful solution to break this cycle, fostering a more equitable financial system. By leveraging comprehensive financial data, lenders can identify creditworthy individuals who were previously excluded.

Alternative Data Integration: Utilizing rental payments, utility bills, and other non-traditional data for credit assessment.

Tailored Product Offerings: Developing credit products specifically designed for thin-file or credit-invisible populations.

Reduced Bias: Potentially mitigating biases inherent in traditional credit scoring models by focusing on actual financial behavior.

Empowered Consumers: Giving individuals more control over their financial narrative and access to essential services.

Ultimately, the expansion of Open Banking will lead to a more accessible credit market, enabling more people to secure loans for homes, education, or small businesses, thereby contributing to broader economic growth and stability. This move towards data-driven inclusion is a key benefit that will materialize more fully by 2026.

Challenges and Considerations for Widespread Adoption

While the benefits of Open Banking are clear, its widespread adoption in the US is not without its challenges. The fragmented nature of the US financial system, coupled with concerns around data privacy and security, presents significant hurdles that need to be addressed proactively. Overcoming these obstacles will be crucial for realizing the full potential of Open Banking by 2026.

One of the primary concerns revolves around data security. With more data flowing between various entities, the risk of cyberattacks and data breaches increases. Building robust security protocols and ensuring consumer trust in these systems will be paramount. Financial institutions must invest heavily in cybersecurity infrastructure and transparent communication about data handling practices.

Navigating Data Privacy and Security

Consumer trust is the bedrock of Open Banking. Without confidence that their data is being handled securely and ethically, consumers will be reluctant to grant access. This necessitates clear regulatory guidelines, strong enforcement, and a commitment from all participants to prioritize data protection.

Standardized Security Protocols: Developing and enforcing industry-wide security standards for data exchange.

Consumer Education: Informing consumers about their data rights, how data is used, and the security measures in place.

Robust Consent Mechanisms: Ensuring clear, explicit, and easily revocable consent processes for data sharing.

Interoperability Challenges: Harmonizing diverse technological infrastructures across thousands of US financial institutions.

Furthermore, achieving true interoperability across the vast and varied US financial landscape is a complex undertaking. Unlike countries with a few dominant banks, the US has thousands of financial institutions, each with its own legacy systems. Developing common APIs and standards that can accommodate this diversity will require significant collaboration and investment. Addressing these challenges effectively will be key to ensuring a smooth transition to a fully functional Open Banking ecosystem.

The Future of Credit: Personalization and Proactive Solutions

Looking ahead to 2026 and beyond, Open Banking is set to usher in an era of unprecedented personalization and proactive financial solutions in the credit market. The ability to access a comprehensive and dynamic view of a consumer’s financial life will allow lenders to move beyond reactive assessments to offer highly tailored and timely credit products. This shift will benefit both consumers, who receive more relevant offers, and lenders, who can better manage risk.

Imagine receiving a pre-approved loan offer for a home renovation exactly when your savings indicate you’re ready to buy materials, or a small business owner getting access to working capital precisely when their sales data shows a seasonal upturn. These are the types of proactive, value-added services that Open Banking can enable, transforming credit from a transactional service into a strategic financial partnership.

AI and Machine Learning Integration

The true power of Open Banking data will be unleashed through its integration with Artificial Intelligence (AI) and Machine Learning (ML). These technologies can analyze vast datasets to identify subtle patterns, predict future financial behavior, and assess risk with a precision unmatched by traditional methods. This will lead to more intelligent lending decisions and a reduction in defaults.

Dynamic Risk Assessment: Continuously updating credit risk profiles based on real-time financial activity.

Personalized Product Matching: Automatically identifying and offering credit products that align with a consumer’s financial goals.

Fraud Detection Enhancement: Leveraging behavioral patterns to detect and prevent fraudulent activities more effectively.

Automated Financial Advice: Providing proactive recommendations for improving financial health and creditworthiness.

This future vision of credit is not just about faster approvals; it’s about fostering financial wellness. By providing consumers with access to better-matched credit products and proactive financial insights, Open Banking can help individuals and businesses make smarter financial decisions, ultimately leading to greater economic stability and prosperity. The next 12 months will be crucial in laying the groundwork for this transformative future.

Key Aspect

Impact on Credit Decisions

Data Access Expansion

Lenders gain comprehensive view of financial health beyond traditional credit scores.

Financial Inclusion

Credit invisible populations access loans through alternative data assessment.

Personalized Offers

Tailored credit products and proactive financial solutions become standard.

Security & Trust

Robust protocols and consumer education are critical for adoption.

Frequently Asked Questions About Open Banking in the US

What is Open Banking and how does it work in the US?▼

Open Banking allows consumers to securely share their financial data with authorized third-party providers. In the US, it’s driven by regulatory guidance and market innovation, using secure APIs to enable data exchange with explicit consumer consent, fostering new financial services.

How will Open Banking specifically impact credit decisions by 2026?▼

By 2026, Open Banking will provide lenders with a richer, real-time view of an applicant’s financial health, including spending habits and savings. This leads to more accurate risk assessments, personalized credit offers, and reduced reliance on traditional, limited credit scores.

Will Open Banking improve financial inclusion for underserved populations?▼

Yes, significantly. Open Banking enables lenders to consider alternative data like rental and utility payments for ‘credit invisible’ individuals. This broader data set helps assess creditworthiness for those lacking traditional credit histories, fostering greater access to financial products.

What are the main security concerns with Open Banking data sharing?▼

Primary concerns include cyberattacks and data breaches due to increased data flow. Robust security protocols, stringent regulatory oversight, and clear consumer consent mechanisms are crucial to building trust and protecting sensitive financial information.

What role will AI and Machine Learning play in Open Banking credit decisions?▼

AI and ML will analyze vast Open Banking datasets to identify patterns, predict financial behavior, and assess risk with high precision. This integration will lead to dynamic risk assessments, personalized product matching, enhanced fraud detection, and proactive financial advice for consumers.

Conclusion

The trajectory of Open Banking initiatives in the US for 2026: How data sharing will reshape credit decisions in 12 months points towards a more dynamic, equitable, and efficient credit market. The shift from fragmented data to a consensual, holistic view of consumer finances promises to unlock significant value, fostering greater financial inclusion and enabling more personalized financial products. While challenges related to security and interoperability persist, the combined forces of regulatory encouragement and market innovation are poised to overcome these hurdles. The coming year will be instrumental in solidifying the foundations of this new financial paradigm, ultimately empowering consumers and transforming the landscape of credit access and assessment for the better.

A journalism student and passionate about communication, she has been working as a content intern for 1 year and 3 months, producing creative and informative texts about decoration and construction. With an eye for detail and a focus on the reader, she writes with ease and clarity to help the public make more informed decisions in their daily lives.