VantageScore 4.0: New Credit Score Models Gaining Traction in US for 2026

VantageScore 4.0 is rapidly gaining traction in the US credit market, poised to significantly reshape how creditworthiness is assessed by 2026, offering a more inclusive and dynamic evaluation than previous models.

Por: Maria Eduarda em 28 de outubro de 2025

Última atualização em: 26 de junho de 2026

Advertisements

VantageScore 4.0 is rapidly gaining traction in the US credit market, poised to significantly reshape how creditworthiness is assessed by 2026, offering a more inclusive and dynamic evaluation than previous models.

Advertisements

The financial landscape in the United States is continuously evolving, and a significant shift is underway with New Credit Score Models (VantageScore 4.0) Gaining Traction in the US for 2026: A Comparative Analysis. This emerging model promises to redefine how lenders assess risk and how consumers understand their financial standing, necessitating a closer look at its features and implications.

understanding the shift to VantageScore 4.0

The credit scoring ecosystem in the US has long been dominated by FICO, but a new contender, VantageScore 4.0, is steadily gaining ground. This model represents a significant evolution, moving beyond static snapshots of credit history to incorporate more dynamic data points, offering a potentially fairer assessment for a broader spectrum of consumers. Its increasing adoption by lenders, particularly by 2026, suggests a pivotal change in how creditworthiness will be evaluated across various financial products.

VantageScore 4.0 is designed to be more inclusive, aiming to score more consumers than older models, including those with limited credit histories. This is achieved through its sophisticated algorithms that analyze a wider array of data, making it a crucial development for both consumers seeking credit and lenders looking to expand their reach responsibly.

what makes VantageScore 4.0 different?

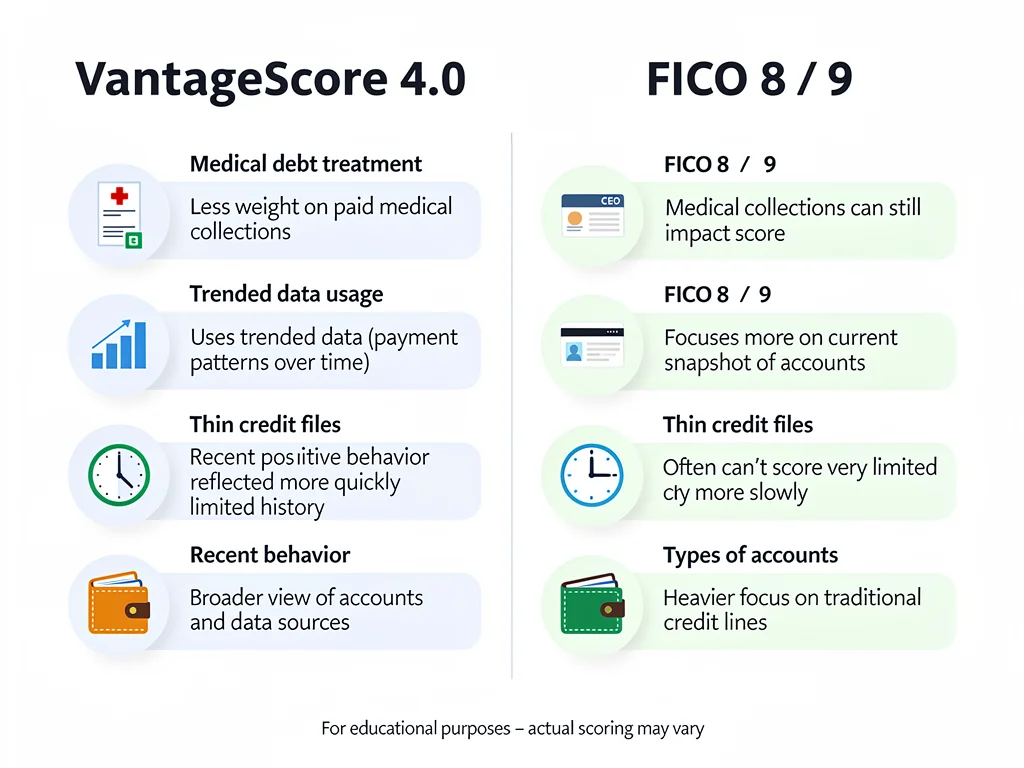

Trended Data: Unlike traditional models that primarily focus on current outstanding balances, VantageScore 4.0 analyzes payment trends over time. This means it looks at whether your balances are increasing, decreasing, or remaining stable, offering a more nuanced view of your financial behavior.

Medical Collections: It treats paid medical collection accounts differently, giving them less weight than unpaid ones, and excludes medical collections under a certain threshold, which can be beneficial for consumers burdened by healthcare costs.

Public Records: Tax liens and civil judgments are no longer factored into the score, providing a cleaner slate for individuals who have resolved these issues.

The shift towards VantageScore 4.0 reflects a broader industry movement towards more predictive and equitable credit assessment. By leveraging advanced analytics, it aims to provide lenders with a clearer picture of an applicant’s financial habits, potentially leading to more accurate lending decisions and greater access to credit for underserved populations. Understanding these fundamental differences is key to navigating the evolving credit landscape effectively.

comparative analysis: VantageScore 4.0 vs. FICO models

To truly appreciate the significance of VantageScore 4.0, it’s essential to compare it with the long-standing FICO models. While both aim to predict credit risk, their methodologies and the data they emphasize can lead to different scores for the same individual. This divergence is critical for consumers, as the specific model used by a lender can influence their eligibility and terms for loans, credit cards, and other financial products.

FICO models, particularly FICO Score 8 and 9, have been the industry standard for decades. They rely heavily on payment history, amounts owed, length of credit history, new credit, and credit mix. While effective, they have faced criticism for sometimes being less accommodating to diverse financial situations, such as those with limited credit files or significant medical debt.

key distinctions in scoring methodology

One of the most profound differences lies in the use of trended data by VantageScore 4.0. FICO models typically consider the current balance reported on your credit accounts. In contrast, VantageScore 4.0 analyzes a 24-month history of balances and payments. This means it observes whether you’re consistently paying down debt or if your balances are creeping up, offering a more dynamic risk assessment.

Another notable distinction is how medical collections are handled. FICO Score 9, a more recent FICO iteration, lessened the impact of paid medical collections, but VantageScore 4.0 goes further by completely ignoring medical collections that have been fully paid. This approach aims to prevent medical emergencies from disproportionately harming an individual’s credit standing, recognizing that medical debt often arises from unforeseen circumstances rather than irresponsible financial behavior.

impact on credit access and financial inclusion

The differences extend to how thin credit files are handled. Both models can score individuals with limited credit history, but VantageScore 4.0 is designed to be more effective at doing so, often requiring less data to generate a score. This can be a game-changer for young adults, recent immigrants, or anyone new to credit, potentially opening doors to financial products previously out of reach.

Ultimately, the choice between VantageScore 4.0 and various FICO models often depends on the specific lender and the type of credit being sought. While FICO still holds a dominant market share, the increasing adoption of VantageScore 4.0 by major lenders and credit bureaus signals a growing acceptance of its alternative, and often more inclusive, approach to credit risk assessment.

the role of trended data in VantageScore 4.0

The incorporation of trended data is arguably the most revolutionary aspect of VantageScore 4.0. This innovative approach moves beyond a static evaluation of credit accounts, instead analyzing the trajectory of a consumer’s financial behavior over a 24-month period. This allows lenders to gain a deeper, more nuanced understanding of an applicant’s credit habits and their potential for future repayment.

Traditional credit scoring models often present a snapshot, showing current balances and payment statuses. While useful, this can sometimes miss the bigger picture. For instance, a consumer who consistently pays down their credit card balance each month, even if they use a significant portion of their available credit, might be viewed more favorably by a model that considers this trend, as opposed to one that only sees a high utilization rate at a specific point in time.

how trended data improves accuracy

Payment Patterns: It differentiates between consumers who pay their balances in full, those who make minimum payments, and those whose balances are consistently increasing. This provides a clearer indication of financial discipline.

Debt Management: Lenders can identify individuals who are actively working to reduce their debt versus those who are accumulating more, even if both have similar current balances.

Risk Prediction: By observing these patterns, VantageScore 4.0 can make more accurate predictions about future repayment behavior, leading to better risk assessment for lenders.

For consumers, understanding the importance of trended data means that consistent, responsible financial behavior will be even more critical. It encourages not just on-time payments, but also actively managing and reducing debt over time. This dynamic scoring method rewards positive financial habits that might have been less explicitly recognized by older models.

The integration of trended data signifies a move towards a more sophisticated and forward-looking credit assessment. It provides a richer narrative of a consumer’s financial journey, allowing for more precise and potentially more favorable credit decisions for those who exhibit strong, consistent credit management practices.

impact on consumers: what to expect by 2026

As VantageScore 4.0 continues its widespread adoption, especially by 2026, consumers in the US can anticipate several significant changes in how their creditworthiness is perceived and how they interact with the credit market. These changes will necessitate a proactive approach to credit management and a deeper understanding of the factors influencing their scores.

One of the most immediate impacts will be on credit access. The model’s ability to score more consumers, including those with thin credit files, could open doors for individuals previously denied loans or credit cards. This inclusivity is particularly beneficial for younger demographics, recent immigrants, and those who have historically been marginalized by traditional scoring methods.

preparing for the new credit landscape

Monitor All Scores: Consumers should regularly check both their FICO and VantageScore scores, as different lenders may use different models. Understanding both will provide a comprehensive view of their credit standing.

Focus on Trended Behavior: Beyond just making on-time payments, actively working to reduce credit card balances over time will be more visibly rewarded by VantageScore 4.0. Consistent debt reduction signals lower risk.

Understand Medical Debt Rules: Be aware of how paid and unpaid medical collections are treated. Resolving medical debts can have a more positive impact on your VantageScore than on some older FICO versions.

The emphasis on trended data means that a sustained pattern of responsible financial behavior will be more heavily weighted. This encourages consumers to adopt long-term strategies for debt management rather than focusing solely on short-term fixes. For example, consistently paying more than the minimum on credit cards will likely lead to a better VantageScore.

Furthermore, the exclusion of tax liens and civil judgments means that past financial difficulties of this nature will not perpetually hinder an individual’s credit opportunities, provided these issues have been resolved. This provides a pathway for financial rehabilitation that might have been less clear under previous models. Consumers should educate themselves on these nuances to optimize their credit profiles.

advantages for lenders and the broader economy

The growing adoption of VantageScore 4.0 isn’t just beneficial for consumers; it also presents significant advantages for lenders and the broader US economy. By providing a more accurate and inclusive assessment of credit risk, this new model can foster a healthier lending environment, expand market opportunities, and potentially reduce overall risk for financial institutions.

Lenders using VantageScore 4.0 gain access to a more predictive tool that can help them identify creditworthy applicants who might have been overlooked by older models. This is particularly true for individuals with thin credit files or those whose financial history might not fit neatly into traditional scoring parameters. By scoring more consumers, lenders can responsibly expand their customer base.

economic benefits and risk mitigation

Expanded Market Reach: Lenders can extend credit to a wider segment of the population, including those historically underserved, which can stimulate economic activity and growth.

Reduced Default Rates: The enhanced predictive power of trended data allows for more precise risk assessment, potentially leading to lower default rates for lenders as they make more informed decisions.

Improved Portfolio Management: With a more dynamic view of consumer behavior, lenders can better manage their existing loan portfolios, identifying potential risks or opportunities more effectively.

The ability of VantageScore 4.0 to leverage trended data means that lenders can distinguish between temporary financial fluctuations and sustained patterns of behavior. This deeper insight allows for more granular risk pricing, meaning that individuals with strong trended data might qualify for better interest rates or more favorable loan terms, while those with deteriorating trends could be identified for early intervention.

From an economic perspective, greater financial inclusion can lead to increased consumption, investment, and overall economic stability. When more people have access to credit, they can pursue education, purchase homes, start businesses, and make other investments that contribute to economic prosperity. VantageScore 4.0’s role in facilitating this access could be a key driver of economic growth in the coming years.

challenges and considerations in adoption

While VantageScore 4.0 offers numerous benefits, its full integration into the US credit market by 2026 is not without its challenges and considerations. The transition from established FICO models requires significant adjustments from lenders, regulators, and consumers alike. Understanding these hurdles is crucial for a smooth and effective shift.

One primary challenge is the sheer inertia of the existing system. FICO models have been deeply embedded in lending practices, underwriting systems, and regulatory frameworks for decades. Changing these systems to accommodate a new scoring model involves substantial IT infrastructure updates, training for lending personnel, and validation processes to ensure compliance and accuracy.

navigating the transition period

Lender Adaptation: Financial institutions need to invest in new technologies and processes to integrate VantageScore 4.0, which can be costly and time-consuming. This includes updating loan origination systems and risk assessment algorithms.

Regulatory Acceptance: While VantageScore 4.0 has gained significant traction, full regulatory acceptance across all lending categories, particularly in areas like mortgage lending, is an ongoing process.

Consumer Education: There’s a vital need to educate consumers about how VantageScore 4.0 works, how it differs from FICO, and what they can do to improve their scores under this new model. Misinformation or lack of understanding could lead to confusion.

Another consideration is the potential for score discrepancies. Because VantageScore 4.0 uses different methodologies, a consumer’s score might vary significantly between a FICO model and a VantageScore model. This can create confusion and frustration if consumers are not aware of which model a particular lender is using.

Furthermore, data availability and consistency across all three credit bureaus (Experian, Equifax, and TransUnion) are critical. While VantageScore is a joint venture of these bureaus, ensuring that all necessary trended data is consistently collected and reported by creditors is an ongoing effort. Overcoming these challenges will be key to the successful and widespread adoption of VantageScore 4.0 by 2026.

strategies for credit success with VantageScore 4.0

As VantageScore 4.0 becomes an increasingly prevalent factor in US credit decisions by 2026, consumers must adapt their credit management strategies to align with its unique methodology. Proactive steps can help individuals maximize their scores and leverage the benefits of this evolving model, ensuring continued credit access to favorable credit opportunities.

A fundamental strategy involves understanding the emphasis on trended data. This means moving beyond merely paying on time and focusing on actively reducing credit card balances over time. Consistently showing a downward trend in debt, even if starting from a higher utilization, can be more beneficial under VantageScore 4.0 than simply maintaining a high balance without significant pay-downs.

actionable tips for a strong VantageScore 4.0

Consistent Debt Reduction: Make it a priority to pay more than the minimum on revolving credit accounts. The long-term trend of decreasing balances will positively impact your score.

Manage Medical Debt Prudently: While paid medical collections are less impactful, striving to pay off medical debts promptly can still demonstrate financial responsibility and prevent them from becoming a negative factor.

Diversify Credit Responsibly: A healthy mix of credit (e.g., installment loans and revolving credit) can be beneficial, but only if managed responsibly. Avoid opening too many new accounts in a short period.

Regularly Review Credit Reports: Check your credit reports from all three bureaus for errors. Disputing inaccuracies is crucial, as even small mistakes can affect your score.

Another crucial aspect is maintaining a long and positive credit history. While VantageScore 4.0 can score thin files, established accounts with a history of responsible payments always contribute positively. Avoid closing old, well-managed accounts, as this can shorten your credit history and potentially impact your score.

Ultimately, the core principles of good credit management remain: pay your bills on time, keep credit utilization low, and only borrow what you can comfortably repay. However, with VantageScore 4.0, these principles are viewed through a more dynamic lens, rewarding sustained positive financial behavior. By adopting these strategies, consumers can position themselves for optimal credit success in the evolving financial landscape of 2026 and beyond.

Key Aspect

Brief Description

Trended Data

Analyzes 24-month payment and balance history for dynamic risk assessment.

Medical Debt

Paid medical collections are ignored; unpaid ones have less impact than FICO.

Inclusivity

Scores more consumers, including those with thin credit files, expanding access.

Public Records

Ignores tax liens and civil judgments, providing a cleaner credit slate.

frequently asked questions about VantageScore 4.0

What is the main difference between VantageScore 4.0 and older FICO models?▼

The primary distinction is VantageScore 4.0’s use of trended data, analyzing a 24-month history of payments and balances. This offers a more dynamic view of credit behavior compared to FICO’s more static snapshot of current account statuses.

How does VantageScore 4.0 treat medical debt?▼

VantageScore 4.0 completely ignores paid medical collection accounts. It also gives less weight to unpaid medical collections compared to other types of debt, aiming to reduce the negative impact of unforeseen healthcare costs on credit scores.

Will my credit score be different with VantageScore 4.0?▼

Yes, your score could likely be different. Due to its unique methodology, especially the reliance on trended data and different treatment of certain negative items, your VantageScore 4.0 might vary from your FICO score. It’s advisable to check both.

How can I improve my VantageScore 4.0?▼

Focus on consistent debt reduction, paying more than the minimum on credit cards to show a positive trend. Also, ensure on-time payments, keep credit utilization low, and manage medical debts promptly to reflect responsible financial behavior.

Why is VantageScore 4.0 gaining traction in the US?▼

Its enhanced predictive power, greater inclusivity for thin credit files, and more nuanced treatment of certain debts make it attractive to lenders seeking a broader and more accurate assessment of credit risk, driving its adoption by 2026.

conclusion

The emergence and increasing adoption of New Credit Score Models (VantageScore 4.0) Gaining Traction in the US for 2026: A Comparative Analysis mark a pivotal moment in the American credit landscape. This shift signifies a move towards more dynamic, inclusive, and predictive credit assessments, benefiting both consumers through expanded access to credit and lenders through more accurate risk evaluation. By understanding its core features, particularly the emphasis on trended data and the differential treatment of medical debt, consumers can strategically manage their credit to thrive in this evolving financial environment. The continued integration of VantageScore 4.0 promises to reshape financial opportunities and foster a more equitable credit ecosystem across the United States.

A journalism student and passionate about communication, she has been working as a content intern for 1 year and 3 months, producing creative and informative texts about decoration and construction. With an eye for detail and a focus on the reader, she writes with ease and clarity to help the public make more informed decisions in their daily lives.