Credit Card Extended Warranty Changes 2026: What You Need to Know

Significant changes to credit card extended warranty perks are set to take effect by January 2026, impacting consumer protection on purchases and requiring cardholders to review their benefit strategies.

Por: Lucas Bastos em 23 de janeiro de 2026

Última atualização em: 26 de junho de 2026

Advertisements

Significant changes to credit card extended warranty perks are set to take effect by January 2026, impacting consumer protection on purchases and requiring cardholders to review their benefit strategies.

Are you relying on your credit card for an extra layer of protection on your purchases? If so, pay close attention: an important alert: changes to credit card extended warranty perks effective January 2026 (recent updates) are on the horizon, poised to significantly alter how you approach consumer protection. This shift could impact everything from electronics to major appliances, making proactive understanding essential for every savvy cardholder.

Advertisements

The Evolving Landscape of Credit Card Benefits

Credit card benefits have long been a key differentiator for consumers choosing between various financial products. Beyond rewards points and cash back, perks like extended warranties offered a valuable safety net, promising repairs or replacements for eligible purchases beyond the manufacturer’s guarantee. These benefits were often a silent but powerful advantage, providing peace of mind and tangible savings for cardholders.

However, the financial industry is dynamic, constantly adapting to economic pressures, regulatory changes, and evolving consumer behavior. Over the past few years, we’ve witnessed a gradual but steady erosion of some of these once-standard protections. Many issuers have quietly scaled back or eliminated certain benefits, leaving cardholders unaware until they needed to file a claim. This trend is now culminating in a more significant, industry-wide adjustment concerning extended warranties, with a clear deadline set for January 2026.

Why the Shift in Extended Warranty Policies?

Several factors contribute to these widespread changes. Increased costs for card issuers to maintain these benefits, coupled with a desire to streamline offerings and focus on more frequently utilized perks, play a significant role. Furthermore, the rise of third-party extended warranty providers and evolving consumer purchasing habits might also influence these decisions. Issuers are re-evaluating the value proposition of each benefit, prioritizing those that resonate most with their target demographics while managing their operational expenses.

Cost Management: The expense of processing claims and covering repairs for defunct items has become substantial for issuers.

Benefit Streamlining: Banks are simplifying their benefit portfolios to focus on core offerings and popular rewards.

Market Dynamics: The proliferation of alternative warranty solutions and shifts in consumer purchasing behavior influence issuer decisions.

Regulatory Scrutiny: While not always direct, the broader regulatory environment can prompt banks to review their financial commitments.

Understanding these underlying reasons helps contextualize the forthcoming changes. It’s not merely an arbitrary decision but a strategic move by financial institutions to adapt to a changing market and optimize their product offerings. For consumers, this means a need to re-evaluate their reliance on these benefits and explore alternative protection strategies.

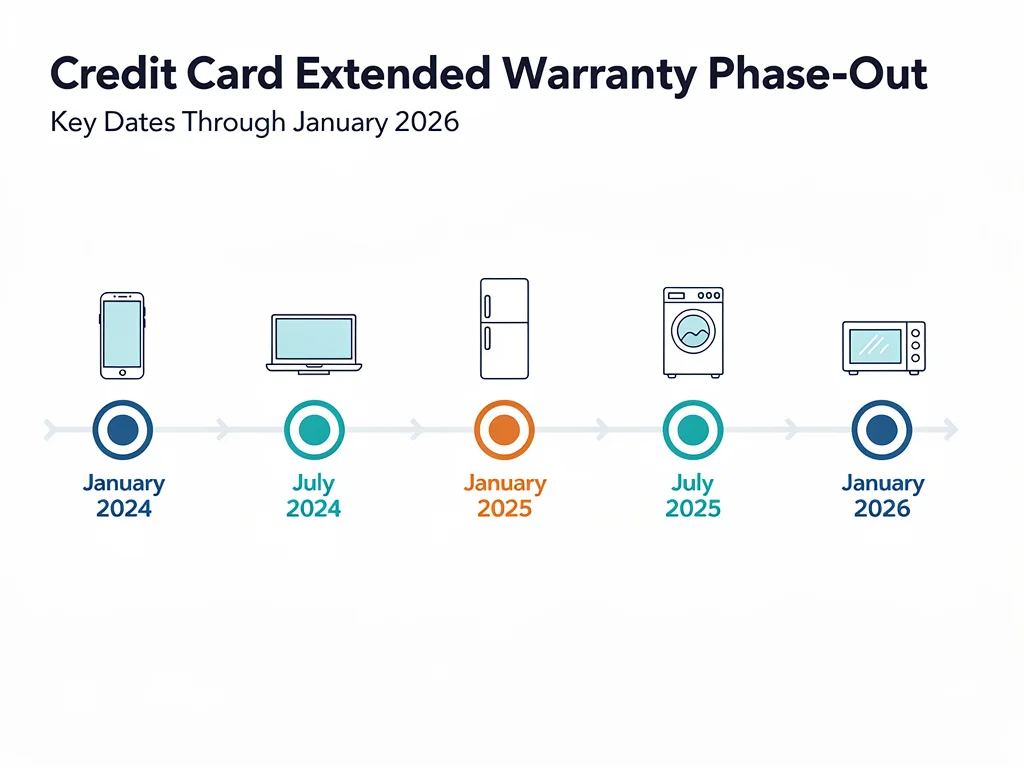

What Exactly is Changing by January 2026?

The core of the upcoming modifications revolves around the discontinuation or significant reduction of extended warranty benefits across a broad spectrum of credit cards. Historically, many premium credit cards, particularly those from major networks like Visa, Mastercard, and American Express, offered an automatic extension of the manufacturer’s warranty, often by an additional year. This benefit applied to eligible purchases made with the card, providing an invaluable safety net for unexpected product failures.

By January 2026, many of these blanket extended warranty policies will either cease to exist or become significantly more restrictive. While the exact details will vary by issuer and specific card product, the general trend indicates a move away from automatic, comprehensive coverage. Some cards may eliminate the benefit entirely, while others might introduce tighter claim limits, shorter extension periods, or exclude certain product categories.

Impact on Specific Card Networks and Issuers

While no single announcement covers all cards, industry insiders and recent trends suggest that the changes will be widespread. Major issuers like Chase, Citibank, Bank of America, and American Express have all made adjustments to various benefits in recent years, and extended warranties are a prime target for further modification. Mastercard and Visa, which often dictate baseline benefits for their networks, have also indicated shifts, leaving individual banks to interpret and implement these changes for their co-branded and proprietary cards.

Visa: Many Visa Signature and Infinite cards previously offered extended warranty. Expect significant reductions or eliminations.

Mastercard: World Elite Mastercard benefits, including extended warranty, are also subject to review and potential cuts by issuers.

American Express: Amex has already scaled back some purchase protections, and further adjustments to extended warranties are probable.

Discover: Discover cards generally had fewer extended warranty offerings, but any existing ones could be affected.

Cardholders are strongly advised to consult their specific card’s guide to benefits, which is usually available online through their issuer’s website or via their mobile banking app. This document is the definitive source for understanding the precise terms and conditions that will apply to their cards post-January 2026. Ignoring these updates could lead to unpleasant surprises when a product fails and the expected protection is no longer available.

Who Will Be Most Affected by These Changes?

The upcoming changes to credit card extended warranty perks will disproportionately affect certain groups of consumers. Primarily, individuals who frequently purchase high-value electronics, appliances, and other goods that typically come with a manufacturer’s warranty will feel the most significant impact. These are the consumers who have historically relied on their credit cards to provide an extra layer of protection, extending the lifespan of their investments without incurring additional costs.

Small business owners who use personal or business credit cards for equipment purchases may also find themselves in a more vulnerable position. The loss of an automatic extended warranty could mean higher out-of-pocket expenses for repairs or replacements, potentially affecting their operational budgets. Furthermore, consumers who are less financially savvy or those who do not regularly review their credit card benefits might be caught off guard, discovering the absence of this perk only when they need it most.

Products and Purchases at Risk

Virtually any item that comes with a standard manufacturer’s warranty could be affected. This includes a wide range of consumer goods that many people purchase regularly. The value of the extended warranty often correlated directly with the cost and complexity of the item, making it particularly valuable for more expensive purchases.

Electronics: Laptops, televisions, smartphones, cameras, and gaming consoles.

Home Appliances: Refrigerators, washing machines, dishwashers, and ovens.

Power Tools: Drills, saws, and other workshop equipment.

Small Kitchen Appliances: Blenders, coffee makers, and toasters.

For these types of purchases, the extended warranty provided by credit card issuers often served as a critical backup. Without it, consumers will either need to budget for potential future repairs, purchase separate extended service plans, or simply accept the risk of product failure once the manufacturer’s warranty expires. This shift necessitates a more conscious approach to how purchases are protected and financed.

Strategies to Mitigate the Impact of Warranty Changes

With the impending changes to credit card extended warranty perks, it’s crucial for consumers to develop proactive strategies to protect their purchases. Simply hoping for the best is no longer a viable option, especially for significant investments. Fortunately, several alternatives exist that can help bridge the gap left by the diminished credit card benefits, ensuring your valuable items remain covered.

The first step is always to be informed. Regularly check your credit card issuer’s website or contact their customer service to get the most up-to-date information on your specific card’s benefits. Don’t assume that benefits will remain constant; financial institutions are not always proactive in notifying cardholders of benefit reductions. Once you understand what you’re losing, you can then explore the most suitable alternative protection methods for your lifestyle and purchasing habits.

Exploring Alternative Protection Options

When credit card extended warranties become less reliable, other forms of protection become more prominent. These alternatives often come with their own costs and considerations, but they offer tailored coverage that can be essential for high-value items.

Manufacturer’s Extended Warranties: Many manufacturers offer their own extended service plans at the point of sale. While these come at an additional cost, they are often comprehensive and specifically designed for the product.

Third-Party Extended Warranty Providers: Companies specializing in extended warranties offer coverage for a wide range of products. Research reputable providers and compare their plans, deductibles, and coverage limits.

Homeowner’s/Renter’s Insurance: For certain items, especially major appliances or electronics that are part of your home’s contents, your homeowner’s or renter’s insurance policy might offer some protection against specific perils, though typically not against mechanical breakdown.

Retailer-Specific Protection Plans: Large retailers often have their own protection plans, which can be convenient to purchase alongside the item. Evaluate these carefully against third-party options.

Careful consideration of these options is paramount. Compare costs, coverage terms, deductibles, and the claims process for each. Sometimes, the cost of an extended warranty might outweigh the potential benefit, especially for lower-cost items. For expensive purchases, however, an alternative protection plan could be a wise investment, providing peace of mind similar to the historical credit card benefit.

Reviewing Your Current Credit Card Portfolio

The impending changes in credit card extended warranty perks present an opportune moment for all cardholders to conduct a thorough review of their entire credit card portfolio. It’s no longer sufficient to simply accumulate cards based on sign-up bonuses or initial rewards rates. A holistic understanding of each card’s long-term value, including its diminishing or changing benefits, is now more critical than ever.

Start by listing all your credit cards and identifying the specific benefits each one currently offers, particularly focusing on purchase protection, extended warranties, and return protection. Then, cross-reference this information with the latest updates from your card issuers regarding changes effective January 2026. This exercise will help you pinpoint which cards are losing valuable perks and which might still retain some level of protection, albeit potentially altered.

Optimizing Your Card Usage for Remaining Benefits

Once you have a clear picture of your updated benefits landscape, you can start optimizing your card usage. This might involve shifting certain types of purchases to cards that still offer the protections you value, or even considering new cards that align better with your current needs, even if they come with an annual fee.

Prioritize Cards with Retained Benefits: For purchases where an extended warranty is critical, use the card that still offers the most robust coverage, if any.

Consider Premium Cards: Some ultra-premium cards, despite potential adjustments, might retain more generous benefits compared to standard cards. Evaluate if the annual fee is justified by the remaining perks.

Diversify Protection: Instead of relying on a single card, consider a strategy where different cards offer different types of protection, or combine card benefits with third-party warranties.

Re-evaluate Annual Fees: If a card’s annual fee was justified by its extended warranty benefit, and that benefit is now gone or significantly reduced, it might be time to downgrade or cancel the card.

This strategic review is not a one-time event. The credit card benefits landscape is constantly shifting, so making it a habit to periodically assess your cards and their associated perks will ensure you’re always maximizing their value and adapting to new industry standards. Staying informed and agile in your credit card strategy is key to navigating these changes successfully.

The Future of Credit Card Perks and Consumer Protection

The changes to credit card extended warranty perks effective January 2026 are indicative of a broader trend within the financial industry. As traditional benefits become less sustainable for issuers, the focus is shifting towards perks that either have a lower cost to provide or offer a more direct, quantifiable value to a wider range of cardholders. This means consumers can expect to see an evolution in what credit cards offer as a primary incentive.

We might see an increased emphasis on travel-related benefits, concierge services, identity theft protection, and personalized offers that leverage data analytics. Cash-back programs and rewards points will likely remain central, but even these could see adjustments in how they are earned and redeemed. The goal for issuers is to create benefit packages that are attractive enough to retain customers while remaining financially viable in the long term.

What to Expect in the Coming Years

Looking ahead, consumer protection will likely become a more complex, multi-layered responsibility. Relying solely on a single credit card for all ancillary benefits may no longer be a prudent strategy. Instead, individuals will need to actively seek out and combine various forms of protection to ensure their purchases and financial well-being are adequately safeguarded.

Increased Personal Responsibility: Consumers will need to be more diligent in researching and purchasing separate protection plans for valuable items.

Rise of Specialized Insurance Products: Expect to see more tailored insurance options for specific categories like electronics or home appliances.

Focus on Digital Security: Benefits related to cybersecurity, fraud protection, and identity theft will likely grow in importance and prevalence.

Personalized Benefits: Card issuers may move towards more customizable benefit packages, allowing cardholders to choose perks that align with their spending habits.

The landscape of credit card benefits is undeniably transforming. While some beloved perks may fade, new ones will undoubtedly emerge. The key for consumers will be to remain adaptable, continuously educate themselves on their card’s offerings, and strategically combine various protection methods to maintain a robust safety net for their purchases and financial life. The era of passive benefit reliance is giving way to one of active and informed consumer choices.

Communicating with Your Credit Card Issuer

In light of the significant changes to credit card extended warranty perks effective January 2026, clear and proactive communication with your credit card issuer is paramount. Many cardholders often overlook the importance of direct engagement with their financial institutions, assuming that all necessary information will be automatically provided or easily found. However, benefit changes can be complex, and the specifics often vary even within the same card network.

Do not wait until you need to file a claim to discover that a benefit has been altered or eliminated. Make it a point to reach out to your issuer well in advance of the January 2026 deadline. This could involve checking their official website for updated guides to benefits, looking for specific notifications in your monthly statements, or, ideally, contacting customer service directly to ask targeted questions about your card’s extended warranty policy and any upcoming modifications.

Key Questions to Ask Customer Service

When you contact your credit card issuer, be prepared with specific questions to ensure you get the most accurate and relevant information. Generic inquiries might yield generic responses, so aim for clarity and detail in your questions. This direct approach can save you time and potential frustration down the line.

What specific changes are being made to the extended warranty benefit on my [Card Name] card? Inquire about the exact date the changes take effect and if any purchases made before that date will still be honored under the old terms.

Will the extended warranty be completely removed, or will there be modifications to its terms, such as coverage limits or duration? Understand if the benefit is being scaled back or eliminated entirely.

Are there any alternative purchase protection benefits replacing the extended warranty, or are there other cards you offer that still provide similar coverage? Explore if your issuer has other products that meet your needs.

Where can I find the most up-to-date guide to benefits for my card? Request a direct link or a mailed copy of the revised terms and conditions.

Document your conversations, noting the date, time, and the name of the representative you spoke with. This record can be invaluable if any discrepancies or misunderstandings arise in the future. Proactive communication ensures you are fully aware of your card’s benefits, allowing you to make informed decisions about your purchases and overall financial strategy in a rapidly changing landscape.

Key Point

Brief Description

Effective Date

January 2026 marks the widespread implementation of changes to credit card extended warranty benefits.

Benefit Reduction

Many credit card issuers are eliminating or significantly scaling back their extended warranty offerings.

Consumer Impact

High-value purchases and frequently warranted items will require alternative protection strategies.

Mitigation Strategies

Consider manufacturer warranties, third-party plans, and reviewing your card portfolio for remaining benefits.

Frequently Asked Questions About Extended Warranty Changes

What is the primary reason for these credit card extended warranty changes?▼

The primary reasons include increased costs for card issuers to maintain these benefits, a strategic effort to streamline offerings, and a shift towards more frequently used perks. The financial viability of providing extensive, automatic extended warranties has decreased for many banks, leading to these widespread adjustments across the industry.

How can I find out if my specific credit card is affected by these changes?▼

To determine if your card is affected, you should consult your card’s guide to benefits, typically available on your issuer’s website or mobile app. You can also contact your credit card’s customer service directly and ask about any upcoming changes to extended warranty benefits for your specific card product.

What are the best alternatives to credit card extended warranties?▼

Good alternatives include purchasing manufacturer’s extended warranties, utilizing reputable third-party extended warranty providers, and carefully reviewing retailer-specific protection plans. For certain items, your home insurance policy might offer limited coverage, but this is usually for specific perils, not mechanical breakdowns.

Will purchases made before January 2026 still be covered by the old warranty terms?▼

Generally, purchases made before the effective date of the changes (often January 2026) are expected to be covered under the terms and conditions that were in place at the time of purchase. However, it is crucial to confirm this directly with your credit card issuer, as policies can vary. Always keep records of your purchases and benefit guides.

Are all credit card types losing their extended warranty benefits?▼

While the trend is widespread, not all credit card types will necessarily lose their extended warranty benefits entirely. Some premium cards might retain a modified version, or certain issuers might opt to keep it for specific products. The exact impact varies by issuer and card, necessitating individual verification of your specific card’s benefits.

Conclusion

The impending alert: changes to credit card extended warranty perks effective January 2026 (recent updates) represent a significant shift in the landscape of consumer protection. While the convenience of automatic extended warranties may be diminishing, this evolution compels cardholders to become more proactive and informed about their financial tools. By understanding these changes, exploring alternative protection options, and diligently reviewing your credit card portfolio, you can ensure that your valuable purchases remain safeguarded and your financial strategies are optimized for the future. Staying adaptive and engaged with your credit card issuers will be key to navigating this new era of credit card benefits effectively.

I'm a content creator fueled by the idea that the right words can open doors and spark real change. I write with intention, seeking to motivate, connect, and empower readers to grow and make confident choices in their journey.