Inflation’s Grip: 7.5% Inflation and US Credit Card Rates in 2026

The 7.5% inflation rate in early 2026 is significantly driving up US credit card interest rates, compelling consumers to manage debt more strategically and financial institutions to adjust lending models.

Por: Maria Eduarda em 18 de março de 2026

Última atualização em: 26 de junho de 2026

Advertisements

The 7.5% inflation rate in early 2026 is significantly driving up US credit card interest rates, compelling consumers to manage debt more strategically and financial institutions to adjust lending models.

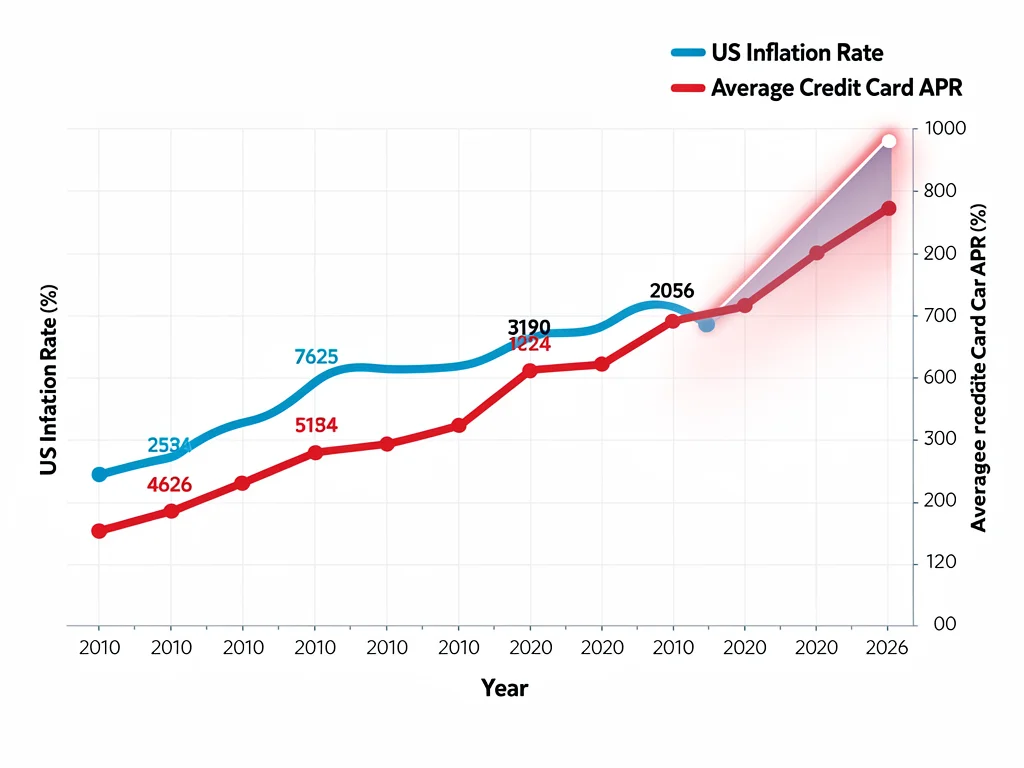

As we navigate early 2026, the specter of a 7.5% inflation rate looms large over the American economy, profoundly influencing various financial sectors. For millions of consumers, one of the most immediate and tangible effects is felt directly in their wallets through mounting credit card interest payments. This expert analysis delves into the impact of current inflation (7.5% in early 2026) on US credit card interest rates, exploring the mechanisms at play and offering insights into what consumers and financial institutions can expect.

Advertisements

Understanding the Inflation-Interest Rate Nexus

The relationship between inflation and interest rates is fundamental to macroeconomic theory. When inflation, such as the 7.5% observed in early 2026, rises persistently, central banks typically respond by increasing benchmark interest rates to cool down the economy and curb rising prices. This action has a ripple effect across all lending products, particularly credit cards.

Credit card interest rates are predominantly variable, meaning they are directly tied to a benchmark rate, most commonly the Prime Rate. The Prime Rate itself is heavily influenced by the federal funds rate, which the Federal Reserve adjusts in response to economic conditions, including inflation. Therefore, a significant jump in inflation almost inevitably translates into higher credit card APRs for consumers.

The Federal Reserve’s Role in Rate Adjustments

The Federal Reserve’s primary mandate includes maintaining price stability. With inflation at 7.5%, the Fed is under considerable pressure to act decisively. Their tools, primarily the federal funds rate, directly impact the cost of borrowing for banks, which then pass these costs on to consumers. This transmission mechanism ensures that an increase in the federal funds rate quickly leads to an increase in the Prime Rate, and subsequently, credit card interest rates.

Federal Funds Rate: The target rate for interbank lending, set by the Federal Reserve.

Prime Rate: The interest rate commercial banks charge their most creditworthy customers, typically 3% higher than the federal funds rate.

Credit Card APRs: Largely determined by adding a margin to the Prime Rate, reflecting the cardholder’s creditworthiness.

In essence, the ongoing inflationary pressures serve as a strong indicator for the Federal Reserve to continue, or even accelerate, its tightening monetary policy. This proactive stance aims to prevent inflation from becoming entrenched, but it comes at the cost of higher borrowing expenses for consumers, particularly those carrying credit card balances.

The Direct Impact on Consumer Finances

For the average American household, a 7.5% inflation rate coupled with rising credit card interest rates presents a formidable financial challenge. The cost of living is already increasing due to inflation, meaning every dollar buys less. Simultaneously, the cost of servicing existing credit card debt becomes more expensive, creating a double-whammy effect.

Consumers who carry a balance month-to-month will notice a significant increase in their minimum payments and the total interest paid over the life of their debt. This can lead to a reduction in disposable income, making it harder to save, invest, or even cover essential expenses. The psychological burden of rising debt can also be substantial, impacting financial well-being and overall quality of life.

Strategies for Managing Higher Rates

Navigating an environment of elevated interest rates requires proactive strategies. Consumers should prioritize paying down high-interest debt, explore balance transfer options, and consider debt consolidation. Understanding the true cost of carrying a balance is more critical than ever.

Prioritize High-Interest Debt: Focus on paying off cards with the highest APRs first to minimize interest accrual.

Balance Transfers: Consider moving high-interest balances to a new card with a 0% introductory APR, if eligible.

Debt Consolidation: Explore personal loans or other consolidation methods to secure a lower, fixed interest rate.

Budget Review: Re-evaluate spending habits to free up more funds for debt repayment.

The cumulative effect of higher inflation and increased credit card rates can push some households into precarious financial situations. It’s crucial for consumers to assess their current debt load and implement a robust repayment plan to mitigate the long-term impact.

Credit Card Issuers’ Response to Inflationary Pressures

Credit card issuers are not immune to the effects of inflation. While higher interest rates can translate to increased revenue from interest payments, they also face rising operational costs and the potential for higher default rates among consumers struggling with debt. Issuers must carefully balance profitability with risk management in this environment.

In response to a 7.5% inflation rate, issuers are likely to continue adjusting their lending models. This could involve stricter underwriting standards for new applicants, particularly those with lower credit scores. They might also re-evaluate credit limits for existing cardholders and offer more targeted financial literacy resources to help customers manage their debt.

Risk Management and Portfolio Adjustments

Financial institutions are keenly aware that sustained high inflation can erode purchasing power and increase the likelihood of consumers defaulting on their obligations. To mitigate this risk, they often undertake a series of strategic adjustments. This includes a more granular analysis of consumer credit health, potentially leading to a tightening of available credit or a reduction in special offers for balance transfers, which become riskier propositions for the issuer when the underlying economic climate is volatile.

Stricter Underwriting: Enhanced scrutiny of credit applications, focusing on income stability and debt-to-income ratios.

Credit Limit Adjustments: Proactive reduction of credit limits for some cardholders to manage exposure to potential defaults.

Product Offerings: Shifting focus towards products with lower perceived risk or those that cater to more creditworthy segments.

Ultimately, credit card issuers are attempting to protect their portfolios against the economic uncertainties brought about by high inflation. While this can be beneficial for their long-term stability, it also means that access to credit may become more challenging and more expensive for a segment of the consumer population.

Economic Outlook and Future Rate Projections

The 7.5% inflation rate in early 2026 is a critical data point that shapes the economic outlook for the remainder of the year and beyond. Economists and financial analysts are closely watching for signs of inflation moderation or acceleration, as this will dictate the Federal Reserve’s future policy decisions and, consequently, credit card interest rates.

Should inflation remain stubbornly high, further rate hikes are almost a certainty. Conversely, if inflationary pressures begin to recede, the Fed might pause or even consider rate cuts, which would offer some relief to borrowers. However, the current environment suggests a continued period of elevated rates as the Fed remains committed to bringing inflation back to its target.

Factors Influencing Future Rate Movements

Several key indicators will influence the trajectory of credit card interest rates. These include employment figures, supply chain stability, geopolitical events, and consumer spending patterns. Each of these elements contributes to the overall inflationary picture and informs the Federal Reserve’s policy decisions.

Employment Data: A strong labor market can contribute to wage growth, potentially fueling inflation.

Supply Chains: Continued disruptions can lead to higher prices for goods and services.

Geopolitical Stability: Global events can impact energy prices and trade, influencing inflation.

Consumer Spending: Robust consumer demand can push prices higher, while a slowdown can temper inflation.

Predicting the future with absolute certainty is impossible, but the current consensus among many experts points to a sustained period of higher interest rates until inflation shows clear and consistent signs of returning to more manageable levels. This means consumers should prepare for credit card rates to remain elevated for the foreseeable future.

The Broader Economic Repercussions

The ripple effect of high inflation and increased credit card interest rates extends beyond individual consumer finances and credit card issuers. It impacts the broader economy, influencing consumer spending, business investment, and overall economic growth. When consumers are burdened with higher debt costs, their discretionary spending often decreases, which can slow economic activity.

Businesses may also find it more expensive to borrow, impacting their ability to invest in expansion, hiring, or innovation. This can create a challenging environment for economic growth, potentially leading to a slowdown or even a recession. The delicate balance between controlling inflation and supporting economic growth is a constant challenge for policymakers.

Impact on Specific Sectors

Certain sectors of the economy are more susceptible to the effects of rising interest rates. For instance, industries reliant on consumer credit, such as retail and automotive, may experience reduced demand as borrowing becomes more expensive. The housing market can also be indirectly affected, as higher interest rates generally make all forms of borrowing less attractive, potentially impacting consumer confidence and their ability to save for down payments.

Retail Sector: Reduced consumer spending due to higher debt service costs.

Automotive Industry: Higher financing costs for vehicle purchases.

Small Businesses: Increased cost of capital for operations and expansion.

Housing Market: Indirect impact through reduced consumer savings and confidence.

The interconnectedness of the financial system means that a significant shift in one area, such as credit card interest rates, can have far-reaching consequences. Understanding these broader repercussions is essential for a holistic view of the economic landscape in an era of high inflation.

Navigating the New Financial Landscape: Advice for Consumers

In this era of 7.5% inflation and elevated credit card interest rates, consumers must adopt a proactive and strategic approach to their personal finances. Simply continuing with old habits will likely lead to increased debt burdens and financial stress. Empowering oneself with knowledge and implementing sound financial practices is paramount.

This means not only understanding how interest rates work but also actively seeking ways to reduce reliance on high-interest credit. Financial literacy becomes a powerful tool, enabling individuals to make informed decisions that protect their financial health in a challenging economic climate. It’s an opportunity to re-evaluate financial goals and build stronger, more resilient financial habits.

Key Steps for Financial Resilience

Building financial resilience in a high-inflation, high-interest-rate environment involves a combination of immediate actions and long-term planning. It’s about taking control of your debt and ensuring your financial foundation is strong enough to withstand ongoing economic pressures. This includes creating a detailed budget, exploring debt management strategies, and building an emergency fund to avoid relying on credit for unexpected expenses.

Create a Detailed Budget: Track income and expenses to identify areas for savings and debt repayment.

Build an Emergency Fund: Aim for at least 3-6 months of living expenses to avoid accruing new debt.

Improve Credit Score: A higher credit score can open doors to better loan terms, even in a high-rate environment.

Seek Professional Advice: Consider consulting a financial advisor for personalized strategies.

By taking these steps, consumers can not only mitigate the negative effects of high credit card interest rates but also position themselves for greater financial stability in the long run. The current economic climate, while challenging, can also serve as a catalyst for positive behavioral changes in personal finance.

Key Aspect

Description

Inflation Rate (Early 2026)

US inflation reached 7.5%, significantly impacting purchasing power and financial markets.

Credit Card Interest Rates

Directly influenced by Federal Reserve actions in response to inflation, leading to higher APRs.

Consumer Impact

Increased cost of living combined with higher debt servicing costs, reducing disposable income.

Mitigation Strategies

Prioritize high-interest debt, consider balance transfers, and review personal budgets.

Frequently Asked Questions About Inflation and Credit Card Rates

How does 7.5% inflation directly affect my credit card’s APR?▼

A 7.5% inflation rate prompts the Federal Reserve to raise benchmark interest rates, like the federal funds rate. Since most credit card APRs are variable and tied to the Prime Rate (which follows the federal funds rate), your credit card’s interest rate will likely increase proportionally, making your debt more expensive.

What can I do to lower my credit card interest payments?▼

To lower interest payments, consider paying down balances on cards with the highest APRs first. You could also explore balance transfer credit cards with a 0% introductory APR or consolidate high-interest debt into a personal loan with a lower, fixed rate, if your credit score allows.

Will my credit limit be affected by high inflation and rising rates?▼

Yes, credit card issuers may become more cautious during periods of high inflation and rising rates. They might implement stricter underwriting standards for new applicants or even proactively reduce credit limits for existing cardholders to mitigate their risk exposure to potential defaults.

Is this high inflation rate expected to continue throughout 2026?▼

While economic forecasts can change, many experts anticipate continued elevated inflation, albeit potentially moderating from 7.5%. The Federal Reserve is committed to bringing inflation down, which suggests a sustained period of higher interest rates until clear signs of price stability emerge, potentially throughout 2026.

How does this impact my ability to get new credit in the future?▼

High inflation and rising rates generally lead to a tighter credit market. Lenders may become more selective, requiring higher credit scores and more stable financial profiles. This could make it more challenging to qualify for new credit cards, loans, or favorable terms in the near future.

Conclusion

The 7.5% inflation rate gripping the US economy in early 2026 presents a significant and multifaceted challenge, particularly concerning credit card interest rates. The direct linkage between Federal Reserve policy responses to inflation and the Prime Rate ensures that consumers holding credit card balances will continue to face elevated borrowing costs. This environment necessitates a heightened sense of financial vigilance and strategic debt management from individuals, while credit card issuers navigate increased operational costs and potential default risks. As the economic landscape continues to evolve, understanding these dynamics and adapting personal finance strategies will be crucial for maintaining stability and mitigating the impact of these challenging financial headwinds.

A journalism student and passionate about communication, she has been working as a content intern for 1 year and 3 months, producing creative and informative texts about decoration and construction. With an eye for detail and a focus on the reader, she writes with ease and clarity to help the public make more informed decisions in their daily lives.