2026 US Predatory Lending: High-Interest Traps (36%+ APR) & Avoidance

The 2026 US predatory lending landscape presents significant high-interest traps, often exceeding 36% APR, which consumers must understand and actively avoid through informed financial decisions and awareness of protective measures.

Por: Maria Eduarda em 6 de janeiro de 2026

Última atualização em: 26 de junho de 2026

Advertisements

The 2026 US predatory lending landscape presents significant high-interest traps, often exceeding 36% APR, which consumers must understand and actively avoid through informed financial decisions and awareness of protective measures.

Advertisements

Are you aware of the financial hazards lurking in the credit market? Understanding the 2026 landscape of US predatory lending: identifying high-interest traps (above 36% APR) and how to avoid them is more critical than ever for safeguarding your financial future.

The evolving nature of predatory lending in 2026

Predatory lending, a practice that strips borrowers of their assets or charges excessive interest rates, continues to evolve in the United States. In 2026, these practices are becoming increasingly sophisticated, leveraging digital platforms and complex financial products to ensnare vulnerable consumers. The core characteristic remains the imposition of unfair, deceptive, or abusive loan terms, often targeting individuals with limited financial literacy or urgent cash needs.

Understanding the current mechanisms of predatory lending is the first step toward protection. Lenders engaging in these practices often obscure the true cost of borrowing through convoluted contracts and hidden fees, making it difficult for borrowers to discern the exploitative nature of the agreement. The digital age has further amplified this challenge, with online lenders operating across state lines, sometimes sidestepping traditional regulatory scrutiny.

Key characteristics of predatory loans

Excessive interest rates: Often exceeding 36% APR, these rates make repayment nearly impossible.

Hidden fees and charges: Unexplained charges that inflate the total cost of the loan.

Aggressive sales tactics: Pressuring borrowers into agreements they don’t fully understand.

Loan flipping: Encouraging repeated refinancing that only benefits the lender.

No consideration of ability to repay: Approving loans without proper assessment of the borrower’s financial capacity.

The legal and regulatory environment surrounding predatory lending is constantly changing, with new laws and enforcement efforts attempting to curb these practices. However, predatory lenders are adept at finding loopholes, necessitating a proactive approach from consumers. Awareness of these evolving tactics is essential for anyone navigating the credit market today.

In conclusion, the 2026 landscape of predatory lending is marked by its adaptability and persistence. Consumers must remain vigilant, educated, and prepared to identify and resist financial products designed to exploit rather than assist. This ongoing battle requires both individual diligence and collective advocacy for stronger consumer protections.

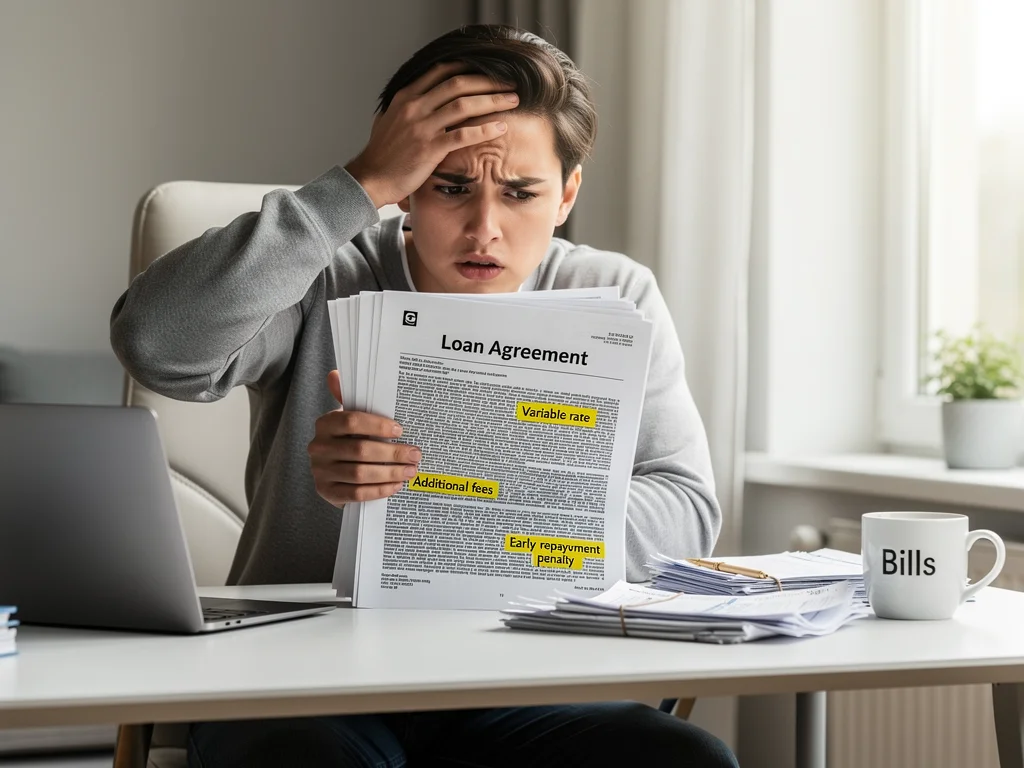

Defining high-interest traps: beyond the 36% APR threshold

The 36% APR threshold is widely recognized by consumer advocates as the demarcation line for predatory lending. While some states have specific caps, this rate is often cited as the point at which a loan becomes financially unsustainable for many borrowers, leading to a cycle of debt. However, identifying high-interest traps involves more than just looking at the stated APR; it requires scrutinizing the entire loan structure.

Beyond the rate, predatory loans often come with terms designed to maximize lender profit at the borrower’s expense. These can include balloon payments, prepayment penalties, and clauses that allow lenders to seize assets without proper legal recourse. The true cost of a loan can be significantly higher than the advertised APR when these additional factors are considered.

Understanding the impact of fees and charges

Many high-interest traps are embedded in the fees. Origination fees, late payment fees, and even fees for simply processing a payment can add up quickly, pushing the effective cost of the loan far beyond the stated APR. These fees are often buried in the fine print of loan agreements, making them easy to overlook for borrowers eager to secure funds.

Origination fees: A charge for processing a new loan application.

Late payment fees: Penalties for missing a payment deadline, often disproportionately high.

Rollover fees: Charges for extending the loan term, common in payday loans.

Prepayment penalties: Fees for paying off a loan early, discouraging responsible financial behavior.

These charges can transform what appears to be a manageable loan into a financial quagmire. A borrower might enter into a loan with a 30% APR, but after factoring in various fees, the effective annual cost could easily soar past 50% or even higher. This hidden cost is a hallmark of predatory lending.

In summary, while the 36% APR serves as a critical benchmark, truly identifying high-interest traps necessitates a deep dive into all aspects of a loan agreement. Consumers must be educated on how fees and hidden charges can inflate the actual cost of borrowing, ensuring they are not caught in a cycle of debt that is difficult to escape.

The primary targets of predatory lenders in the current climate

Predatory lenders do not randomly choose their victims; they strategically target vulnerable populations who are most likely to be desperate for funds and least likely to understand complex financial terms. In 2026, these targets continue to include low-income individuals, minorities, the elderly, and those with poor credit histories. The economic instability experienced by many in recent years has only expanded this pool of at-risk individuals.

These groups often face barriers to accessing traditional credit, making them more susceptible to the allure of quick cash offered by predatory lenders. The promise of immediate relief, even at exorbitant costs, can be incredibly tempting for someone facing an unexpected expense or struggling to make ends meet. Lenders exploit this desperation, offering loans that are often impossible to repay under the given terms.

Demographics most at risk

The data consistently shows that certain demographics are disproportionately affected. For example, communities of color are often targeted with subprime mortgages and high-cost installment loans at higher rates than their white counterparts, even when controlling for income and credit scores. This highlights systemic inequalities that predatory lenders exploit.

Low-income individuals: Limited access to traditional credit and urgent financial needs.

Minority communities: Often subject to discriminatory lending practices.

Elderly citizens: Vulnerable to financial scams and complex agreements.

Individuals with poor credit: Excluded from mainstream lending, forced into high-cost alternatives.

Military personnel: Targeted due to steady income and perception of financial inexperience.

Moreover, the rise of online lending has made it easier for predatory lenders to reach these vulnerable populations, often through targeted advertising on social media and other digital platforms. The anonymity of the internet can also make it harder for consumers to vet lenders and for regulators to track illicit activities.

In concluding this section, it is clear that predatory lenders prey on those in dire financial straits or those with limited access to mainstream financial services. Recognizing these target groups is crucial for developing effective consumer protection strategies and for empowering individuals to resist these harmful practices. Education and access to fair credit alternatives are paramount.

Regulatory landscape and consumer protections in 2026

The regulatory environment governing predatory lending in the US is a complex patchwork of federal and state laws. In 2026, efforts to strengthen consumer protections continue, but challenges persist due to varying state regulations and the rapid evolution of financial products. The Consumer Financial Protection Bureau (CFPB) remains a key federal agency tasked with overseeing consumer financial products and services, including those offered by predatory lenders.

Many states have enacted their own laws to cap interest rates and restrict certain lending practices, such as payday loans and title loans. However, some states have either weaker regulations or no caps at all, creating a fragmented landscape where predatory lenders can thrive in less regulated areas. This disparity often leads to regulatory arbitrage, where lenders operate from states with lax laws to offer high-cost loans nationwide.

Federal and state initiatives

At the federal level, discussions around a national interest rate cap, potentially at 36% APR, continue to gain traction among consumer advocates. Such a measure would standardize protections across all states and significantly curb the most egregious forms of predatory lending. However, strong opposition from the lending industry makes its passage challenging.

CFPB enforcement: Continuously working to enforce existing laws and issue new rules.

State-level caps: Many states have enacted their own usury laws to limit interest rates.

Military Lending Act (MLA): Protects active-duty military members and their dependents from loans with APRs above 36%.

Beyond legislation, consumer protection agencies are increasingly focusing on financial literacy initiatives. By educating consumers about the dangers of high-interest loans and empowering them with the knowledge to make informed decisions, these agencies aim to reduce the effectiveness of predatory tactics. Technology is also playing a role, with some platforms designed to help consumers compare loan offers and identify red flags.

In conclusion, while the regulatory landscape in 2026 is a blend of federal oversight and state-specific laws, the fight against predatory lending is far from over. Continued advocacy for stronger, more uniform consumer protections and enhanced financial education are crucial to shielding vulnerable populations from these exploitative practices.

Strategies to avoid high-interest loan traps

Avoiding high-interest loan traps requires a combination of financial literacy, proactive planning, and careful decision-making. The best defense against predatory lending is not to need it in the first place, but when financial needs arise, knowing how to navigate the options safely is paramount. The goal is to secure necessary funds without falling into a cycle of debt that can be incredibly difficult to escape.

One of the most effective strategies is to build a strong credit score. A good credit score opens doors to traditional, lower-interest loans from banks and credit unions, making predatory lenders less appealing. Regularly checking your credit report and disputing any errors can help maintain a healthy credit profile.

Practical steps for consumers

Before applying for any loan, it’s essential to research the lender thoroughly. Check reviews, look for complaints with the Better Business Bureau or the CFPB, and verify their licensing. A legitimate lender will be transparent about their terms and conditions and will not pressure you into a quick decision.

Improve your credit score: Pay bills on time, keep credit utilization low.

Build an emergency fund: A financial cushion reduces reliance on short-term high-interest loans.

Explore alternatives: Consider credit union loans, community aid programs, or salary advances.

Read the fine print: Understand all terms, fees, and the total cost of the loan before signing.

Seek financial counseling: Non-profit agencies can offer advice and debt management plans.

Another crucial step is to compare loan offers from multiple lenders. Don’t simply take the first offer you receive. By comparing APRs, fees, and repayment terms, you can identify the most favorable option and avoid those with predatory characteristics. Websites and apps designed for loan comparison can be valuable tools in this process.

In summary, avoiding high-interest loan traps is about empowerment through knowledge and careful planning. By improving financial health, exploring all available options, and meticulously scrutinizing loan agreements, consumers can protect themselves from the pitfalls of predatory lending and secure a more stable financial future.

Empowering consumers through financial literacy and alternative credit solutions

Financial literacy is a powerful tool in combating predatory lending. An informed consumer is less likely to fall victim to deceptive practices and more capable of making sound financial decisions. Educational initiatives that teach budgeting, saving, understanding credit scores, and identifying predatory loan characteristics are vital for empowering individuals across all demographics.

These programs often go beyond basic financial concepts, delving into the specifics of loan agreements, the true cost of interest, and the long-term consequences of high-interest debt. By demystifying financial jargon and highlighting common red flags, financial literacy efforts equip consumers with the confidence to challenge unfair terms and seek better alternatives.

Accessing fair and responsible credit

Beyond education, expanding access to fair and responsible credit availability solutions is equally important. Many individuals turn to predatory lenders because they lack viable alternatives. Community development financial institutions (CDFIs), credit unions, and non-profit organizations often offer loans with reasonable terms and supportive financial counseling.

Credit unions: Offer lower interest rates and more flexible terms to members.

CDFIs: Provide affordable financial services to underserved communities.

Small-dollar loans: Some banks are beginning to offer small, short-term loans at lower APRs.

Employer-sponsored programs: Some employers offer emergency loans or salary advances.

Technology also plays a role in connecting consumers with ethical lending options. Fintech companies are developing innovative platforms that use alternative data to assess creditworthiness, potentially offering fair loans to individuals who might be overlooked by traditional lenders. This expansion of responsible credit options can significantly reduce the demand for predatory products.

In conclusion, empowering consumers through comprehensive financial literacy and the promotion of accessible, fair credit solutions is a multi-faceted approach to addressing predatory lending. These efforts not only protect individuals from exploitative practices but also contribute to a more equitable and stable financial system for all.

The future outlook: policy changes and advocacy for 2026 and beyond

The fight against predatory lending is ongoing, and the future outlook for 2026 and beyond hinges on continued policy changes and robust advocacy efforts. While progress has been made, the adaptability of predatory lenders necessitates a dynamic response from lawmakers, regulators, and consumer protection groups. The ultimate goal remains a financial marketplace where all consumers have access to fair, transparent, and affordable credit.

One of the most impactful policy changes would be the implementation of a national interest rate cap at 36% APR. Such a federal standard would eliminate the current patchwork of state laws, providing uniform protection across the country. This would prevent lenders from exploiting regulatory gaps and ensure that no consumer is subjected to exorbitant interest rates, regardless of where they live.

Key areas for future advocacy

Beyond interest rate caps, advocacy groups are pushing for stronger enforcement mechanisms and increased penalties for predatory lenders. This includes giving regulatory bodies more power to investigate and prosecute fraudulent practices, as well as holding online lenders accountable, regardless of their physical location.

National interest rate cap: A uniform 36% APR limit across all states.

Enhanced regulatory oversight: Greater authority for agencies like the CFPB.

Digital platform accountability: Holding online lenders to the same standards as traditional institutions.

Increased funding for legal aid: Providing resources for victims of predatory lending to seek justice.

Data privacy protection: Safeguarding consumer data from misuse by predatory entities.

Another critical area of focus is the promotion of innovative financial technologies that support responsible lending. This includes encouraging the development of fintech solutions that offer transparent, affordable credit to underserved populations, leveraging data responsibly to assess creditworthiness without resorting to predatory terms. Collaboration between technology companies, financial institutions, and consumer advocates will be key to these advancements.

In conclusion, the future of combating predatory lending in 2026 and beyond depends on a concerted effort to enact comprehensive policy changes, strengthen regulatory enforcement, and foster a financial ecosystem that prioritizes consumer well-being. Through sustained advocacy and innovation, a more equitable and secure credit market is an achievable goal for all Americans.

Key Aspect

Brief Description

Predatory Lending Definition

Loans with unfair, deceptive, or abusive terms, often exceeding 36% APR, targeting vulnerable consumers.

High-Interest Traps

Loans with APRs above 36%, often inflated by hidden fees and complex terms, leading to debt cycles.

Consumer Protection

Federal and state regulations, like the MLA and CFPB oversight, aim to curb predatory practices.

Avoidance Strategies

Improve credit, build emergency funds, explore alternatives, read fine print, and seek financial counseling.

Frequently asked questions about predatory lending

What defines a predatory loan in 2026?▼

In 2026, a predatory loan is generally defined by unfair, deceptive, or abusive terms, often featuring an annual percentage rate (APR) exceeding 36%. These loans typically target vulnerable individuals, trapping them in unsustainable debt cycles through hidden fees, aggressive tactics, and a disregard for the borrower’s ability to repay.

Why is the 36% APR threshold significant?▼

The 36% APR threshold is significant because it’s widely recognized by consumer advocates and some federal laws, like the Military Lending Act, as the maximum sustainable rate. Rates above this often make repayment extremely difficult, leading to a debt spiral where borrowers pay more in fees and interest than the original loan amount, without reducing the principal.

Who are the primary targets of predatory lenders?▼

Predatory lenders primarily target vulnerable populations, including low-income individuals, minority communities, the elderly, and those with poor credit histories. These groups often have limited access to traditional credit and may be desperate for funds, making them susceptible to the allure of quick cash despite exorbitant costs and exploitative terms.

What new consumer protections are in place for 2026?▼

For 2026, consumer protections continue to be a mix of federal and state efforts. The CFPB remains active in enforcement, and some states have strengthened their interest rate caps. There’s ongoing advocacy for a national 36% APR cap and increased accountability for online lenders, but regulatory landscapes vary significantly by state.

How can I avoid high-interest loan traps?▼

To avoid high-interest loan traps, improve your credit score, build an emergency fund, and explore alternative, responsible credit options like credit unions. Always read the fine print of any loan agreement, understand all fees, and consider seeking advice from non-profit financial counselors before committing to a loan.

Conclusion

The 2026 landscape of US predatory lending presents a persistent challenge for consumers, characterized by high-interest traps often exceeding 36% APR and sophisticated tactics designed to exploit financial vulnerability. Protecting oneself requires a multi-pronged approach: understanding the evolving nature of these predatory practices, recognizing the specific demographics targeted, staying informed about regulatory protections, and proactively implementing strategies to avoid falling into debt cycles. Ultimately, financial literacy, coupled with access to fair and responsible credit alternatives, remains the most potent defense against predatory lending. Continued advocacy for stronger national policies and enhanced enforcement will be crucial in fostering a more equitable and secure financial future for all Americans.

A journalism student and passionate about communication, she has been working as a content intern for 1 year and 3 months, producing creative and informative texts about decoration and construction. With an eye for detail and a focus on the reader, she writes with ease and clarity to help the public make more informed decisions in their daily lives.